UK Casino ID Verification Checks and Fast Withdrawal Rules

Table of Contents

- Identity Verification Checks for Fast Casino Withdrawals

- Payment and document risk map

- Withdrawals, deposit balance and bonus conditions

- Bank blocks and spending controls

- Questions to ask before uploading documents

- If a problem has already started

- When payment questions are really control questions

- Related guides

- Common questions

- Normal regulated checks

- Payment and document risk map

- Withdrawals and deposit balance

- Bank blocks and spending controls

- If a problem has already started

Identity Verification Checks for Fast Casino Withdrawals

The Gambling Commission’s consumer guidance says licensed online gambling businesses must ask customers to prove age and identity before they can gamble. That is the opposite of the idea that no identity check is automatically better. A business that avoids basic checks may feel easier at first, but it can leave the customer with less confidence about who is handling the account, whether the business is meeting obligations, and what will happen when a withdrawal is requested.

Identity checks can also appear later in a relationship for legitimate reasons, including legal obligations such as anti-money-laundering checks. The important consumer point is timing and clarity. The Gambling Commission explains that a business should not ask for identity evidence as a withdrawal condition if it could reasonably have asked earlier. That does not mean every later check is improper. It means you should read verification terms before depositing, save the terms that applied, and question vague or shifting explanations.

Credit-card gambling is another useful baseline. Relevant Gambling Commission licensees must not accept credit cards for gambling in Great Britain. A site presenting credit-card access as a simple convenience should therefore make you pause and check exactly who regulates the business and what payment route is actually being used. Do not treat a payment option as proof of legitimacy or safety.

Payment and document risk map

| Situation | What may be normal | What needs caution | Better action |

|---|---|---|---|

| Age and identity checks | A licensed online business asks for evidence before gambling. | The business is unclear, the document request is vague, or the site cannot be matched to official records. | Verify the business first and read how data and documents are handled. |

| Withdrawal verification | Further checks may be needed for legal obligations. | ID is first raised only after a withdrawal when the business could have asked earlier. | Save messages, terms and dates; use the complaint route if the issue is not resolved. |

| Payment method claims | Payment options can vary by business and by regulatory setting. | A site promotes unusual access, credit-card gambling or fewer checks as a benefit. | Check the licence position and avoid using payment claims as proof of trust. |

| Customer funds | Licensed businesses disclose how customer money is protected if the business fails. | The wording is missing, unclear or gives the impression of bank-like protection. | Read customer-funds terms before holding a balance. |

| Personal data | Gambling businesses may need to process data for compliance and player protection. | You are asked to send documents to an unidentified business or through unclear channels. | Do not upload documents until the business and its data handling are clear. |

Withdrawals, deposit balance and bonus conditions

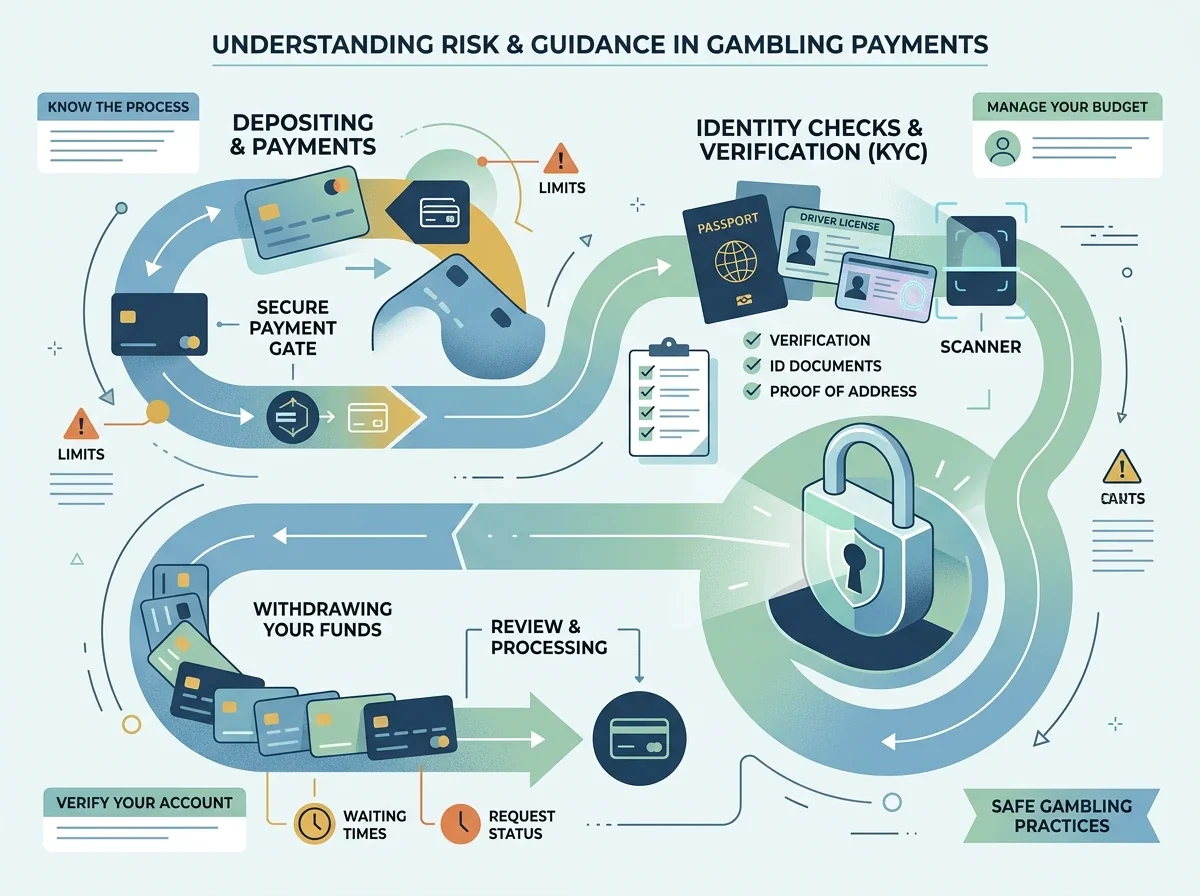

Withdrawal terms should be read before the first deposit. That is when you can still decide not to use the site. Look for the difference between your deposit balance, winnings and funds connected to a bonus. The Gambling Commission’s guidance for licensed operators says players must be informed that they can withdraw their deposit balance at any time, including where a bonus is pending or active, subject to general regulatory obligations. That does not make every later dispute simple, but it gives you a baseline for reading terms.

Bonus-linked funds can add conditions that are easy to miss. A promotion may look simple, while the practical limits are in the full terms: wagering requirements, excluded games, deadlines, maximum bet rules, document checks or restrictions on withdrawing bonus-related winnings. Do not treat a short promotional line as the full agreement. Save the relevant terms when you deposit, because terms can change and a later complaint is easier to explain when you have evidence of what you saw.

If a withdrawal is delayed, avoid making another deposit to “unlock” the situation unless you have clear, verified terms that explain what is happening. Additional deposits can make the record more complicated and can increase harm if gambling is already difficult to control. A better route is to collect evidence, ask the business for a clear explanation, and use the complaint process if the answer is not adequate.

Bank blocks and spending controls

Many banks offer gambling payment blocks, but the details differ. Some tools may take time to activate or remove, and features vary by bank. The important point is that blocks are there to support control, not to be treated as obstacles. If you have set a gambling block, or someone close to you has encouraged you to set one, looking for a payment route that avoids it is a warning sign that the issue is no longer just about payment convenience.

There are also regulatory checks that may look unfamiliar to customers. For covered remote licensees, financial vulnerability checks apply at a current threshold based on deposits minus withdrawals exceeding £150 in a rolling 30-day period from 28 February 2025. This is not a spending cap and not a guarantee that gambling is affordable. It is a regulatory context that helps explain why financial or account checks can appear in licensed settings.

If spending control is the real concern, combine tools rather than relying on one barrier. Bank blocks, gambling-blocking software, GAMSTOP details, support services and debt guidance can work together. Support pages from GamCare, GambleAware, the NHS, MoneyHelper and Citizens Advice explain practical ways to reduce harm and deal with gambling-related money pressure.

Questions to ask before uploading documents

- Who is receiving the document? Identify the legal business and compare it with official records before sending sensitive information.

- Why is the document needed? The reason should be understandable and connected to age, identity, payment, security or legal obligations.

- When could the check have been requested? If a check appears only after a withdrawal, keep a record of when the business first asked and what its terms said.

- How is the document submitted? Avoid unclear channels, personal email addresses or requests that do not appear in the site’s official process.

- What happens if you do not provide it? Read the terms and ask for a clear explanation before sending more money.

These questions do not replace legal advice or a formal complaint. They are practical safeguards. Personal documents are valuable, and a gambling account is not worth handing them to an unclear business.

If a problem has already started

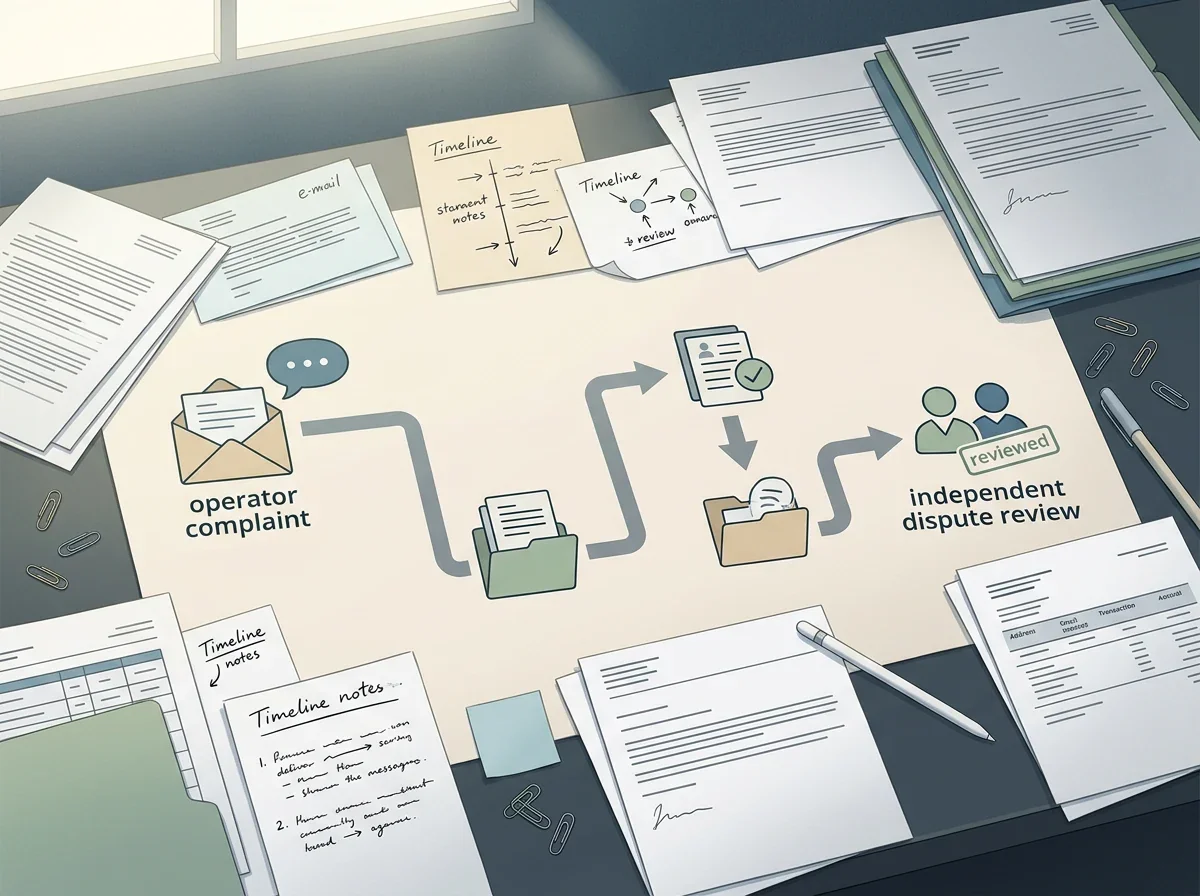

If your account is locked, a withdrawal is delayed or the business is giving changing explanations, switch from pre-use checking to evidence keeping. Save the account history, transaction details, messages, identity-check requests, terms, screenshots and dates. For licensed operators, the usual route is to complain to the business first. If the complaint is unresolved after the relevant period or a deadlock position is reached, the Gambling Commission’s guidance explains the ADR route where eligible.

Do not assume the regulator will recover money for you, and do not rely on threats or pressure tactics. A clear record is more useful than anger. The dedicated guide on withdrawal delays and complaints covers this route in more detail.

If an operator refuses to process your legitimate winnings, you must know how to handle withdrawal delays and complaints to protect your rights.

When payment questions are really control questions

Payment issues are sometimes a sign of a wider problem. If you are trying to use a new route because GAMSTOP, a bank block or another limit is stopping gambling, the safer next step is support. If gambling is affecting debt, mood, work, sleep or relationships, visit GamCare, GambleAware, the NHS gambling help page, MoneyHelper or Citizens Advice. You do not need to wait for the worst possible outcome before using help.

Related guides

- How to check an online gambling site before you deposit explains business and official-record checks.

- What “not on GAMSTOP” means explains the scheme boundary and protection gap.

- Self-exclusion, blocking tools and getting help focuses on controls rather than payment access.

We always advise players to choose platforms that are fully transparent, as highlighted on the CasinoFreeNoGamstop homepage.

Common questions

Is fewer verification always better?

No. In licensed online gambling, age and identity checks are part of the regulatory baseline. Fewer checks can mean less clarity, not less risk.

Can a business ask for documents at withdrawal?

Further checks can be needed for legal obligations, but a business should not use a withdrawal as the first point to ask for evidence it could reasonably have requested earlier. Keep records if this becomes a dispute.

Do bank blocks work the same everywhere?

No. Many banks offer gambling blocks, but features differ. Check your own bank’s process and do not treat a block as something to work around.

Creado por la redacción de «Casino not on Gamstop».